Back when rates were super low during the pandemic, we refinanced down to a 15-year for essentially the same monthly payment we were paying on a 30-year, but which would save us something like half of our total mortgage cost over the life of the loan between the lower rate and the shorter term.

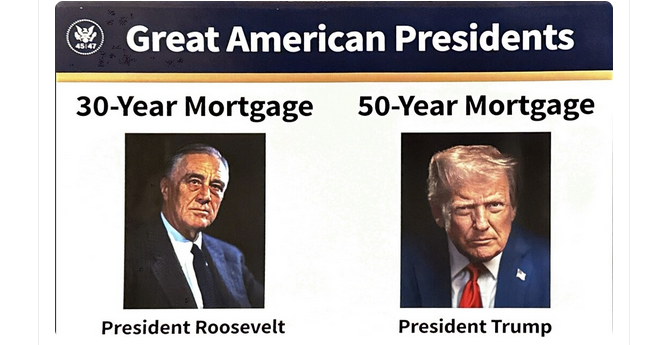

Obviously that’s not really an option anymore, but the idea of a 50-year mortgage does make my mind reel in a similar way. Your monthly payment on a 50-year might be a couple hundred dollars lower than on a 30, but I guarantee not even close to enough to make a meaningful difference. But you will, undoubtedly, end up paying way more in interest over the life of the loan. Maybe even as much as double the principal in interest alone.

I can think of only a few very tiny edge cases where a 30-year would benefit the buyer, and they’re only marginal benefits for people like house flippers.

In the vast majority of cases, a 50-year mortgage can only benefit the lender.

Back when rates were super low during the pandemic, we refinanced down to a 15-year for essentially the same monthly payment we were paying on a 30-year, but which would save us something like half of our total mortgage cost over the life of the loan between the lower rate and the shorter term.

Obviously that’s not really an option anymore, but the idea of a 50-year mortgage does make my mind reel in a similar way. Your monthly payment on a 50-year might be a couple hundred dollars lower than on a 30, but I guarantee not even close to enough to make a meaningful difference. But you will, undoubtedly, end up paying way more in interest over the life of the loan. Maybe even as much as double the principal in interest alone.

I can think of only a few very tiny edge cases where a 30-year would benefit the buyer, and they’re only marginal benefits for people like house flippers.

In the vast majority of cases, a 50-year mortgage can only benefit the lender.