The anarchist cookbook is famous, but you’re probably better off with the declassified tm 31-210 improvised munitions handbook.

It’s like the difference between sex and porn

Even better: The Anarchist Cookbook, nonviolent bait and switch edition:

From the cofounder of Food Not Bombs, an action-oriented guide to anarchism, social change, and vegan cooking

Unlike the original Anarchist Cookbook, which contained instructions for the manufacture of explosives, this version is both a cookbook in the literal sense and also a “cookbook” of recipes for social and political change.

Those dudes are awesome

Yeah, it’s honestly a great book I really recommend reading it

On top of that, the writer of The Anarchist Cookbook went full fash

deleted by creator

Thanks for the link, though I am probably on a list now.

If we all make 50 zines of this handbook and pass them around, we have plausible deniability when The Thingtm happens

This is why I have posted the pdf in every group chat that I’m in.

I’m going to be honest with you it’s a one and three hop no matter what you do if someone of interest no someone who knows someone who knows someone you know you’re on that list anyway and it’s statistically impossible for that not to happen so congratulations you’re on the list with us which is everyone that’s why we all carry smartphones so they can track US easier yay!

I figure if I’m going to be on a list I might as well download it for later use. Hell, I’m a convincing enough liar I probably can explain it’s to prepare for invasion from (whoever we’re told to fear at that time).

Ingredients

1x Pipe

1x BombThanks for that “draw the rest of the fucking owl” recipe

It’s not technically wrong

you might say it’s a ‘cartoon’ of a recipe.

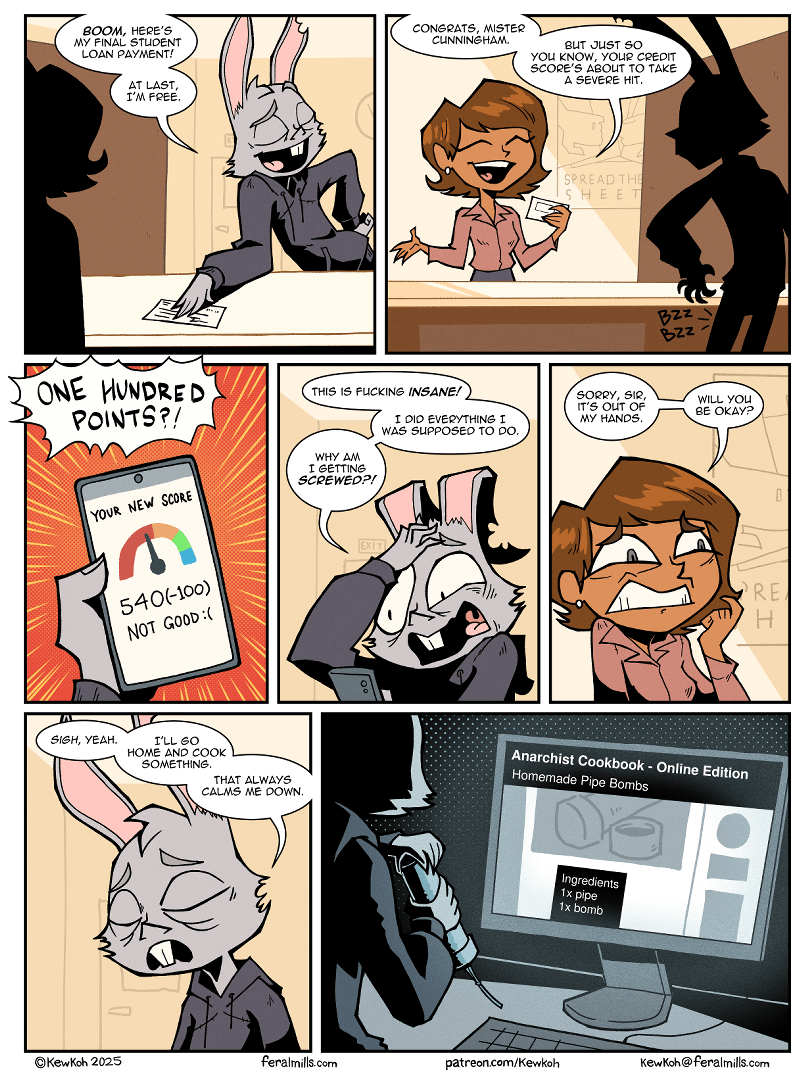

My credit score dropped about 40 points when I paid off my last student loan, but in less than six months it rebounded. Don’t be concerned with temporary dips unless you’re planning on immediately taking out more credit.

Exactly this.

People think they are getting punished, like the bank doesn’t want you to take out another loan. The reality is that it is just an algorithm that sees major events like that and realizes that sometimes paying off a loan and immediately getting a new loan makes you more of a risk not less of one.

The score is a snapshot on a single day of how the algorithm thinks you could handle more credit than you currently have (it is used to apply for new credit), and if you paid off a loan and proceeded to walk into the bank days later to get right back into debt that is clearly/statistically a red flag.

The problem is people see the score like their current value as a person, but the score was designed for loan applications not for you to monitor month to month.

It’s not the bank trying to punish you it is just an algorithm that frankly has very limited data (no concept of assets, only sees statement balances, usually doesn’t include utilities/rent and many other bills) on your actual capability to pay off a loan.

Having worked with lenders before, I can tell you that when they are doing a hard pull, they’re often not even looking at the algorithm score; they might have their own internal algorithm tuned to the factors they care about for whatever financial product, but mostly they’re going to just look at your history as an itemized list. They want to know specifics.

sometimes paying off a loan and immediately getting a new loan makes you more of a risk not less of one.

I think stuff like this is more credit age, student loans are usually the oldest accounts a person will have and resolving that will make your average account age go down.

Possible, especially because there are many different scores, I.e. I believe a car dealers often use a different score than say mortgage underwiters.

But I haven’t had a installment loan of any kind on my credit report for several years and my “average age of accounts” is still reported as excellent. Some revolving accounts in there, but my understanding was that closed accounts don’t leave your report for several years, and continue to count for your average age metric.

There is usually a small penalty for not having “enough types of credit” (if you are like me and don’t have any installment loans), but the reporting sites seem to say that it doesn’t affect the score much, and it took quite a while before they started reporting that as a problem.

I remember my friend telling me I was making a mistake for letting a $1400 medical bill go to collections. They told me my credit score would suffer. I said I didn’t care. I wasn’t trying to get a loan at the moment and I wasn’t trying to impress anyone at the bank. Even if it dipped, I didn’t care.

I think medical collections is one of the few things that has no impact on your credit score, if I remember right.

Either way, your credit score can pretty easily turn around from being absolute shit if your financial situation turns around. I used to have a score of like 400 and now its 700. A lot of creditors still deny me based on the stupid shit I did as a teenager that sent it down to 400, but once it gets back towards 700 (assuming you have income to back applications) theres always some place that will give you a loan on decent terms. For a while there I was shit out of luck on that though and couldnt get a loan from anyone that wasnt predatory

Also a good reason not to pay.

I guess but they can still prepare to burn the whole thing down.

Remember when they screamed and yelled about China’s “social credit score” and how they would use it to oppress their citizens who wouldn’t submit to brainwashing and that they used it to keep people in poverty and how the whole country was a sham and none of the infrastructure they were building was real and they were just trying to save face while running away with all the money?

Every accusation is a confession.

What’s a credit score matter if you don’t need credit.

Some jobs will run your credit during hiring or promotions/role changes

Damn that’s fucked up.

I don’t mean to be out here defending credit scores as a concept, but mine never dropped. Not when I paid off individual student loan accounts, not when the US Federal loans came due after the pandemic pause and I paid them off in one lump sum either. Not when I paid off mybcsr loan either.

Technically the 3 companies that do these each have their own proprietary blend, but it is generally accepted that there are 5 C’s to credit. Character, capacity, capital, collateral, and conditions (“Character” woukd be better described as “history” but that ruins the memnonic).

Which one of these would be negatively impacted by paying off a student loan? None of them! In fact, it improves your Character to pay off a loan successfully, and it improves your capacity to reduce your monthly minimum payments. For stuff like a car loan, paying that off improves your Collateral.

Every single time I have met anyone claiming that paying off a debt hurt their credit score, their story falls apart when I start asking questions. Oh it was actually not them, but a friend of a friend of a friend. Or maybe they also got in a fender Bender and added $3k to their credit card balance that month. Or paying off the debt and the decline in credit score were seperated by months.

What CAN happen is that some accounts only report credit history upon closure. My wife used to work for an “alternative energy supplier” where this was the case. Due to state protections they could not turn off electricity during the winter. People would rack up electric bills for 4 months without paying, then get their electric shut off and suddenly see a huge drop on their credit score out of nowhere. I have heard similar stories of landlords not reporting late rent payments for years until the tenant moves out. This was all years ago though so I’m nkt even sure if that’s true anymore.

{kind=link}